Introduction

Buying property in Malaysia involves more than just paying the purchase price. Many buyers—especially first-time buyers—often underestimate the total cost involved, which can lead to financial strain or unexpected expenses during the transaction.

In addition to the property price, buyers must account for costs such as stamp duty, legal fees, loan charges, valuation fees, and other related expenses. These costs can add up significantly, particularly for higher-value properties.

Understanding the full cost structure is essential for proper financial planning. For example, stamp duty alone can be one of the largest upfront expenses, and it varies depending on the property value and buyer profile.

In this guide, we break down all the costs involved in buying property in Malaysia in 2026, with clear explanations and examples to help you budget accurately.

What Are the Costs of Buying Property in Malaysia?

When purchasing property in Malaysia, the total cost typically includes:

- Property price (main cost)

- Stamp duty on property transfer

- Legal fees for conveyancing

- Loan-related costs (if financing is used)

- Valuation fees

- Insurance (MRTA / MLTA)

- Maintenance fees (for strata properties)

Each of these components plays a role in the overall financial commitment, and some must be paid upfront before ownership is transferred.

Stamp Duty in Malaysia (Biggest Cost)

Stamp duty is one of the most significant costs when buying property in Malaysia. It is charged on the transfer of ownership (Memorandum of Transfer or MOT).

Property Stamp Duty Rates

Stamp duty is calculated using a progressive rate:

| Property Value | Rate |

|---|---|

| First RM100,000 | 1% |

| Next RM400,000 | 2% |

| Next RM500,000 | 3% |

| Above RM1,000,000 | 4% |

Example Calculation (RM1.5 Million Property)

- First RM100,000 × 1% = RM1,000

- Next RM400,000 × 2% = RM8,000

- Next RM500,000 × 3% = RM15,000

- Remaining RM500,000 × 4% = RM20,000

Total Stamp Duty = RM44,000

For a detailed breakdown, you can refer to this stamp duty Malaysia guide to understand how it is calculated in detail.

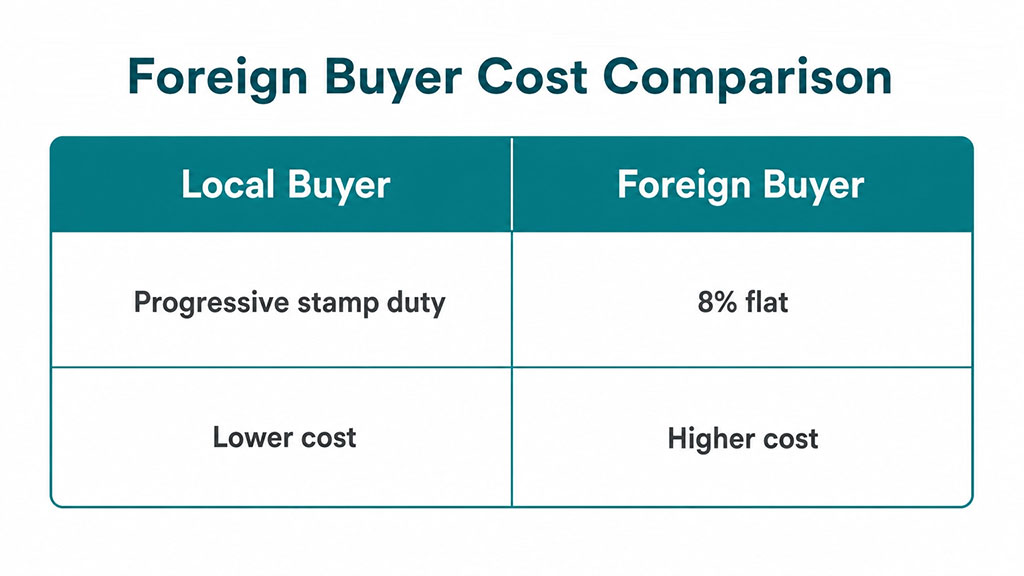

Stamp Duty for Foreign Buyers (2026)

Foreign buyers are subject to different rules. From 2026, residential property purchases by foreigners are subject to a flat 8% stamp duty, which significantly increases the cost of acquisition.

For example:

- RM1,500,000 property → RM120,000 stamp duty

Legal Fees for Buying Property in Malaysia

Legal fees are charged for preparing and handling the Sale and Purchase Agreement (SPA) and other legal documents.

These fees are regulated under the Solicitors Remuneration Order (SRO) and follow a tiered structure.

Legal Fee Scale

| Property Price | Fee |

|---|---|

| First RM500,000 | 1% |

| Next RM500,000 | 0.8% |

| Next RM2,000,000 | 0.7% |

Example Legal Fee Calculation (RM1 Million Property)

- First RM500,000 × 1% = RM5,000

- Next RM500,000 × 0.8% = RM4,000

Total Legal Fees = RM9,000

Note: Additional disbursements (e.g., filing fees, searches) may apply.

Loan Costs and Financing Fees

If you are taking a housing loan, there are additional costs to consider.

Loan Agreement Stamp Duty

- Typically 0.5% of the loan amount

Example:

- RM500,000 loan → RM2,500 stamp duty

Bank Fees

- Processing fees

- Documentation charges

Valuation Fees

Banks require a property valuation before approving a loan. Fees depend on property value but are usually a few hundred to a few thousand ringgit.

Insurance (MRTA / MLTA)

- Mortgage Reducing Term Assurance (MRTA)

- Mortgage Level Term Assurance (MLTA)

These protect the loan in case of death or disability.

Real Property Gains Tax (RPGT)

Although RPGT does not apply when buying property, it is important to understand it for future planning.

RPGT is a tax charged when you sell a property and make a profit. The rate depends on how long you hold the property.

You can refer to this RPGT Malaysia guide to understand how it works.

Other Costs to Consider

Beyond the main costs, buyers should also budget for:

- Agent commission (if applicable)

- Renovation and furnishing costs

- Maintenance fees (for strata properties)

- Utilities setup costs

These costs vary widely depending on the property and buyer preferences.

Total Cost Example (RM1,000,000 Property)

Here is a simplified breakdown of total upfront costs:

| Cost Component | Estimated Amount |

|---|---|

| Stamp Duty | RM24,000 |

| Legal Fees | RM9,000 |

| Loan Stamp Duty | RM2,500 |

| Valuation & Misc | RM2,000 |

| Total Estimated Cost | ~RM37,500+ |

👉 This shows that buyers need significantly more than just the property price.

Cost of Buying Property for First-Time Buyers

First-time buyers are often more sensitive to upfront costs.

Key considerations:

- Budget for at least 3%–5% extra on top of property price

- Understand loan eligibility before committing

- Avoid over-leveraging

Cost for Foreign Buyers in Malaysia

Foreign buyers typically face higher costs due to stricter rules.

Key differences:

- 8% stamp duty on residential property

- Higher minimum purchase thresholds (RM1M–RM2M+)

- Additional approval requirements

Because of this, total acquisition costs are significantly higher compared to local buyers.

You can learn more in this foreigner buying property in Malaysia guide for a full breakdown of rules, minimum prices, and approval requirements.

Common Mistakes Buyers Make

Only Budgeting for Property Price

Many buyers overlook additional costs such as stamp duty and legal fees.

Ignoring Stamp Duty

Stamp duty is one of the largest upfront costs and must be planned early.

Forgetting Legal and Loan Costs

Legal fees and loan-related charges can add thousands to the total cost.

Not Calculating Total Upfront Cost

Buyers should estimate all costs before committing to avoid cash flow issues.

FAQs About Property Buying Costs in Malaysia

How much cash do I need to buy a house in Malaysia?

Typically, buyers should prepare at least 3%–5% of the property price for upfront costs, excluding down payment.

What is the biggest cost besides property price?

Stamp duty is usually the biggest additional cost when buying property in Malaysia, followed by legal fees and loan-related charges. The total amount depends on the property value and financing arrangement.

How much salary do you need to buy a RM500K house in Malaysia?

Generally, buyers need a household income of around RM5,000–RM8,000 per month to qualify for a housing loan for a RM500,000 property, depending on loan tenure, interest rate, and existing financial commitments.

Are legal fees negotiable?

Legal fees are regulated, but some discounts may be offered depending on the law firm.

How much is the lawyer fee to buy a house in Malaysia?

Lawyer fees for buying a house in Malaysia are based on the property price and follow the Solicitors Remuneration Order (SRO). As a general estimate, legal fees are usually around 1% for the first RM500,000 of the property value, with lower rates applied to higher amounts.

For example, legal fees for a RM500,000 property are typically around RM5,000, excluding disbursements and taxes.

Conclusion

The cost of buying property in Malaysia goes far beyond the purchase price. From stamp duty and legal fees to loan-related charges and additional expenses, buyers must be fully prepared to manage these costs.

Proper planning is essential to avoid surprises and ensure a smooth transaction. By understanding each cost component and calculating your total budget in advance, you can make more informed decisions when purchasing property. Besides, there are still a few Malaysia Home Financing Assistance Programmes introduced by Government. Don’t forget to check out them as well to make sure you find the best schemes.

Before committing to a purchase, it is always advisable to consult a qualified lawyer or property professional to ensure that all costs are properly accounted for.