Introduction

For most young Malaysians, the wall between renting and owning isn’t the monthly instalment — it’s the down payment. A standard 10% deposit on a RM450,000 property is RM45,000 in cash, before legal fees, stamp duty, and moving costs. For someone earning RM4,500 a month with PTPTN, rent, and family obligations to manage, saving that amount can take five to seven years. By then, the property is RM550,000.

This is exactly what Skim Rumah Pertamaku (SRP) — also known as My First Home Scheme — was built to solve. Run by Cagamas SRP Berhad, a subsidiary of Malaysia’s national mortgage corporation, the scheme allows eligible first-time buyers to borrow up to 110% of the property price, eliminating the down payment entirely and covering most of the upfront fees as well.

In 2026, SRP is still one of the most valuable financing options for first-time buyers in Malaysia, especially when combined with Budget 2026 incentives like the extended stamp duty exemption and the expanded SJKP guarantee. This guide explains everything you need to know: how it works, who qualifies, which banks participate, and the honest trade-offs to consider before applying.

What Is Skim Rumah Pertamaku (SRP)?

Skim Rumah Pertamaku (SRP) is a government-supported home financing program that was first introduced in Budget 2011 and launched in March of the same year. Cagamas SRP Berhad, a subsidiary of Cagamas Berhad, administers it. Cagamas Berhad has supported Malaysia’s housing finance system since 1986.

The scheme doesn’t lend money directly. Instead, Cagamas SRP serves as a mortgage guarantor for participating banks. If a bank approves a home loan for an SRP-eligible buyer above the standard 90% margin, Cagamas SRP guarantees the extra portion (from 90% to 110%). This guarantee reduces the bank’s risk associated with higher-margin lending, making them more willing to offer financing that they might not approve on their own

In practical terms, the bank lends you up to 110% of the property price. You are responsible for the entire amount, and Cagamas SRP guarantees the bank for anything above 90%.

Why Was SRP Created?

The scheme was designed around a specific affordability problem that persists and may have worsened over the 14 years since its launch.

Property prices have risen faster than income. As of Q1 2025, Malaysia’s median house price was about RM486,070, while the median monthly household income was still below RM6,500. The gap between what most Malaysians earn and what most homes cost makes traditional down payment saving nearly impossible for young workers.

Down payments are the biggest barrier. For any property over RM300,000, the 10% deposit can total tens of thousands of ringgit. Banks tightened lending after 2014, requiring stricter documentation and lower debt service ratios. This made the deposit hurdle even higher for young buyers without family financial support.

Home ownership rates among Malaysians under 35 remained stagnant. Despite government initiatives, the proportion of first-time buyers in the residential market is still below the targets set by housing policy. The SRP program was developed — and remains — one of the government’s main tools to close that gap.

How Does SRP Work?

The mechanics are simple but worth understanding before you apply, because the 110% financing isn’t free money. It’s a higher loan amount you’ll service for up to 35 years.

The Bank Lends, Cagamas Guarantees

Here’s the structure in plain terms:

- You apply for a home loan at a participating bank (Maybank, CIMB, RHB, Bank Islam, BSN, and others).

- The bank assesses you under standard underwriting — income, CCRIS, debt service ratio, employment stability.

- If approved under SRP, the bank lends you up to 110% of the property price.

- Cagamas SRP guarantees the portion above 90% — so the bank’s risk is reduced.

- You are liable for the full amount to the bank. Cagamas’s guarantee protects the bank, not you, in case of default.

- You don’t pay anything extra for the guarantee. SRP doesn’t charge a separate fee, and your interest rate is the bank’s standard housing rate.

The full 110% breaks down into 100% for the property itself, plus an additional 10% to cover legal fees, stamp duty, MRTA/MRTT insurance, valuation costs, and other acquisition expenses. This is the part most buyers miss — SRP doesn’t just eliminate the down payment, it covers the upfront fees that normally drain another RM10,000 to RM20,000 in cash.

Example of an SRP Purchase

To make this concrete:

Conventional 90% loan on a RM450,000 property:

- Down payment (10%): RM45,000

- Legal fees and stamp duty: ~RM13,500 (or RM2,250 with first-time buyer exemption)

- MRTA: ~RM4,500

- Valuation, agency, moving costs: ~RM5,000

- Total upfront cash needed: ~RM68,000 (or ~RM57,000 with stamp duty exemption)

SRP 110% loan on the same RM450,000 property:

- Down payment: RM0

- Legal fees and stamp duty: covered by the additional 10% financing

- MRTA: covered by the additional 10% financing

- Valuation: covered by the additional 10% financing

- Total upfront cash needed: ~RM2,000–RM5,000 (booking fee, miscellaneous costs)

The difference is roughly RM55,000–RM65,000 in cash you don’t have to save before buying. That’s the real value SRP delivers.

The trade-off, which we’ll cover in detail later: your monthly instalment is calculated on the larger loan amount, so monthly commitments are 10-20% higher than a conventional 90% loan on the same property.

Who Is Eligible for SRP in 2026?

SRP eligibility rules come directly from Cagamas SRP’s official terms. The criteria are tighter than many summary articles suggest.

Income Requirements

The household income caps are:

- Individual applicant: Gross monthly income up to RM5,000

- Joint applicants (typically married couples): Combined gross monthly income up to RM10,000, with each applicant earning no more than RM5,000

Income is calculated gross — before EPF, SOCSO, and tax deductions. Side income, commissions, freelance earnings, and business income all count if you want them included for affordability assessment.

The RM10,000 joint cap is firm. A couple earning RM6,000 + RM4,500 = RM10,500 combined exceeds the cap and won’t qualify, even if each individual is below RM5,000.

Other Eligibility Requirements

To apply, you must meet all of the following:

- Malaysian citizen. Permanent residents and foreigners do not qualify.

- First-time home buyer. You and your spouse must not have owned residential property anywhere in Malaysia previously — including by inheritance, gift, or joint ownership.

- Age limit. The 2011 rules set the age cap at 35 for application. Some current participating banks extend this to under 40. Since the cap varies by bank, check directly with your chosen bank.

- Maximum age at end of loan tenure: 65 or 70, depending on the bank.

- Owner-occupied property. The home must be your primary residence. Buying to rent out breaches the scheme terms.

- Stable employment. Most participating banks require minimum 6 months with current employer and confirmed (not probationary) status. Self-employed applicants must provide at least 12 months of business records.

- DSR ceiling. Your total financing obligations (this loan plus existing car loans, personal loans, credit card minimums) cannot exceed 60% of net monthly income. This rule often disqualifies otherwise eligible applicants.

- Clean credit history. No serious defaults, bankruptcy, or major arrears in the past 12 months on your CCRIS and CTOS reports.

The DSR rule deserves attention. A buyer earning RM5,000 net monthly with a RM1,000 car loan instalment has only RM2,000 of remaining DSR headroom for a home loan — which limits the property price you can actually afford regardless of SRP’s 110% financing.

Documents Required

When applying through a participating bank, expect to provide:

- MyKad (front and back) for applicant and spouse if applicable

- Marriage certificate, divorce certificate, or relevant proof (if applicable)

- Latest 3 months’ payslips

- Latest 3 months’ bank statements

- EPF i-Akaun statement (latest)

- Latest EA form or BE income tax form

- CCRIS report (banks pull this directly, but checking yours beforehand helps)

- Sale & Purchase Agreement (SPA) or booking receipt for the property

- For self-employed: SSM business registration, 12 months bank statements, latest tax returns, and Commissioner of Oaths declaration

Banks may request additional documentation depending on your employment type and the specific property.

What Properties Can Be Purchased Under SRP?

The property side of SRP eligibility is more flexible than many buyers realise. The scheme isn’t restricted to a particular development or new launches — secondary market (sub-sale) homes qualify too, as long as the property and the buyer both meet the criteria.

Key Property Criteria

- Maximum property value: RM500,000 (purchase price or open market value, whichever the bank deems lower)

- Location: Anywhere in Malaysia

- Market: Primary (new project) or secondary (sub-sale) — both eligible

- Occupancy: Must be owner-occupied as your primary residence

- Title: Must be a residential title (not commercial, industrial, or mixed-use SOHO/SOVO unless specifically approved)

Eligible Property Types

SRP can be used to finance:

- Apartments and condominiums — including most affordable housing developments in urban areas

- Landed homes — terrace houses, semi-detached, single-storey houses

- Townhouses and serviced residences (if classified as residential)

- PR1MA homes — most PR1MA units fall within the RM500,000 cap, making them SRP-eligible for first-time buyers

- Rumah Selangorku homes — Types A through E all fall well below the RM500,000 cap, allowing eligible first-time Selangor buyers to stack RSKU pricing with SRP financing

- Residensi Wilayah (RUMAWIP) — capped at RM300,000, well within SRP range

For a detailed breakdown of eligibility, income limits, house types, prices and application steps, read our complete guide on Rumah Selangorku 2026 and PR1MA Malaysia 2026.

This stacking is one of SRP’s most underrated features. A Selangor first-time buyer can apply for Rumah Selangorku Type C at RM150,000, then finance the full purchase plus fees with SRP — bringing their upfront cash requirement down to almost zero. Same logic applies to PR1MA buyers and stamp duty exemption.

Participating Banks for SRP Malaysia

SRP is offered through major Malaysian financial institutions. Over the program’s history, more than a dozen banks have participated, and the list shifts as banks adjust their housing loan portfolios.

Banks confirmed as active SRP participants:

- Maybank (including Maybank Islamic)

- CIMB Bank (including CIMB Islamic)

- RHB Bank (including RHB Islamic)

- AmBank (including AmBank Islamic)

- Bank Islam

- BSN (Bank Simpanan Nasional)

- Public Bank

- Hong Leong Bank

- Affin Bank

- Alliance Bank

- OCBC Bank

- HSBC

- Standard Chartered

Each bank’s individual SRP product may differ in terms of interest rate, lock-in period, MRTA structure, and additional eligibility criteria layered on top of the core SRP requirements. It’s worth getting indicative quotes from at least three banks before committing.

Disclaimer: Bank participation and product terms can change. Some banks have temporarily suspended SRP at various points based on internal risk appetite. Before assuming a specific bank participates, verify directly on the Cagamas SRP portal at srp.com.my or contact the bank’s mortgage team.

Budget 2026 Updates Affecting SRP Buyers

Budget 2026 (tabled 10 October 2025) introduced several measures that work alongside SRP to reduce the cost of first-home ownership.

SJKP Expansion to RM20 Billion

The Skim Jaminan Kredit Perumahan (SJKP) was doubled from RM10 billion to RM20 billion, targeting an estimated 80,000 additional first-time home buyers. While SJKP and SRP are separate schemes administered by different agencies, they complement each other:

- SRP is for salaried first-time buyers earning up to RM10,000 joint

- SJKP MADANI is for self-employed, gig workers, and informal sector buyers without traditional payslips

Buyers who don’t qualify for SRP due to irregular income should consider SJKP as an alternative. Read our SJKP MADANI guide for details.

Stamp Duty Exemption Extended to 2027

The 100% stamp duty exemption for first-time Malaysian buyers on properties up to RM500,000 has been extended until 31 December 2027. This is significant for SRP buyers because:

- The RM500,000 stamp duty cap exactly matches the SRP property cap

- Both exemption and SRP target the same first-time buyer profile

- On a RM450,000 home, stamp duty exemption saves around RM11,250 between transfer and loan stamp duty

- The savings are real cash — not just deferred — and reduce the total cost of acquisition

For a buyer using SRP, the stamp duty exemption means you don’t need to use the 10% extra financing to cover stamp duty, which slightly reduces your monthly instalment.

Step-Up Financing Scheme

Budget 2026 also introduced a Step-Up Financing programme for buyers aged 21 to 35. Initial monthly instalments start lower and gradually increase, easing cash flow pressure for early-career individuals. This applies to conventional housing loans and can be combined with SRP at participating banks where available.

LPPSA Ceiling Raised for Civil Servants

The LPPSA (Lembaga Pembiayaan Perumahan Sektor Awam) financing ceiling for civil servants was raised from RM600,000 to RM1 million. Civil servants buying homes priced below RM500,000 can choose between LPPSA financing or SRP through a participating bank. Both options are valid, but it’s worth comparing the different terms.

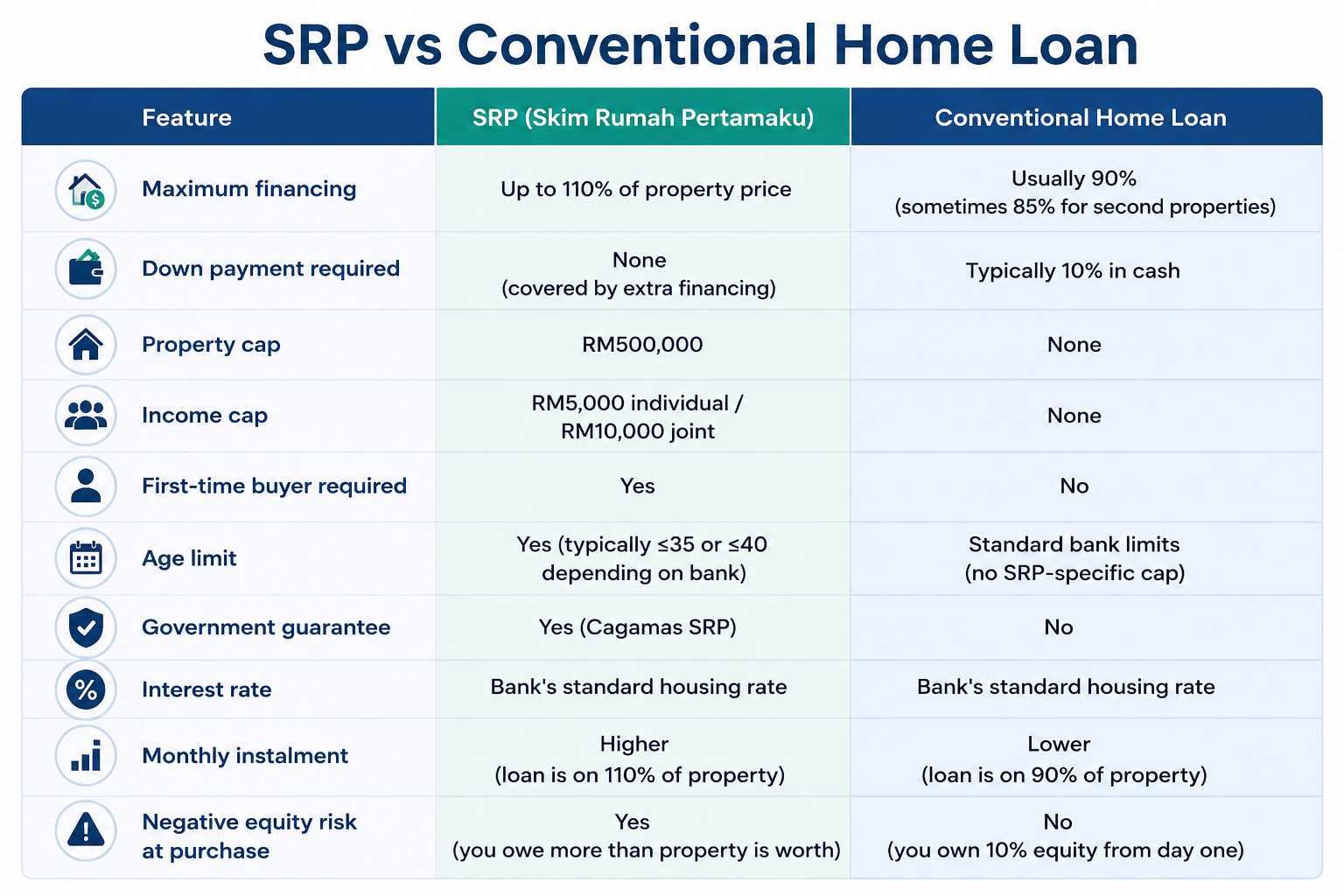

SRP vs Conventional Home Loan

Choosing between SRP and a conventional housing loan is the first decision most eligible first-time buyers face. The differences are significant.

The headline benefit of SRP is clear: no down payment. But the trade-offs are real. Your monthly instalment will be 15-20% higher than a conventional loan on the same property, and you start with negative equity that takes 2-4 years of principal payments and property appreciation to resolve.

For most first-time buyers in 2026, the math still favours SRP — because saving RM50,000+ for a deposit in today’s economy takes years that the property market doesn’t sit still for. But it’s not the default right answer for everyone.

Pros and Cons of Skim Rumah Pertamaku

Pros

No down payment required. This is the main benefit. For young Malaysians without savings, SRP is often the only realistic path to ownership.

Upfront costs covered. The extra 10% above property price includes legal fees, stamp duty (if not exempted), MRTA/MRTT, and valuation. Most buyers only need to pay booking fees upfront.

No additional cost for the government guarantee. You don’t pay Cagamas anything for backing your loan. There are no insurance premium or separate fee — just the bank’s standard interest rate.

Suitable for young professionals and newlyweds. Fresh graduates, young couples, and early-career buyers without family financial support are exactly who SRP was designed for.

Stacking potential. SRP can be combined with the first-time buyer stamp duty exemption, PR1MA pricing, Rumah Selangorku pricing, and EPF Account 2 withdrawals, making multiple subsidies available for a single purchase.

Cons

Income cap limits eligibility. The RM10,000 joint household income limit excludes many M40 Malaysians in dual-income households earning RM12,000-RM15,000 combined.

Larger loan, higher monthly instalment. Borrowing 110% of property value instead of 90% means your monthly commitment is roughly 22% higher than a conventional 90% loan on the same property. Over 35 years, the total interest paid becomes significantly larger.

Negative equity at purchase. When you borrow more than the property is worth, you start in negative equity. If you need to sell within the first 3-5 years due to job relocation, family changes, or marital issues, you’ll need to bring cash to the closing table to cover the gap. This risk is rarely discussed but is real.

Approval is still bank-dependent. SRP eligibility doesn’t guarantee approval. Banks have their own criteria for underwriting, including the 60% DSR rule, employment stability, and credit history. Many SRP-eligible applicants are rejected by banks for affordability issues.

Limited to first-home buyers. Unlike PR1MA (which allows first or second home), SRP is strictly for first-time buyers. If you’ve ever owned residential property, you don’t qualify.

Property cap may not match your local market. In Klang Valley urban areas, RM500,000 buys smaller units or older properties. SRP is of no help if you need a home priced at RM600,000 to RM700,000 for a growing family.

SRP vs PR1MA vs SJKP: Which Is Better?

These three schemes are often confused because they all target first-time buyers — but they’re built for different problems.

| Scheme | Best For | Key Constraint |

|---|---|---|

| SRP (Skim Rumah Pertamaku) | Salaried first-time buyers with limited savings but stable income | Income cap (RM5k/RM10k); first-home only |

| PR1MA Malaysia | Middle-income buyers wanting below-market priced homes | Limited unit availability; balloting required |

| SJKP / SJKP MADANI | Self-employed, gig workers, and irregular income earners | Higher DSR scrutiny; smaller property cap on MADANI variant |

For the full picture of how SRP fits alongside other Malaysian housing programmes — including PR1MA, SJKP MADANI, Rumah Selangorku, Residensi Wilayah, and PPR — see our complete affordable housing schemes Malaysia 2026 guide.

Is SRP Still Worth It in 2026?

Honest answer: yes, for the right buyer.

SRP is genuinely the most powerful tool available for Malaysian first-time buyers who fit the profile — salaried, under RM10,000 joint household income, minimal savings, and looking at properties under RM500,000. For that buyer, the math is straightforward: SRP gets you into ownership 5+ years earlier than conventional saving would, in a market where waiting costs you 4-6% per year in price appreciation.

It’s particularly worth applying if you’re:

- A young professional in your 20s or early 30s building career income

- A newly married couple looking to buy together rather than continue renting

- A first-time buyer with limited savings but stable employment

- An applicant for PR1MA, Rumah Selangorku, or RUMAWIP wanting to maximise financing on top of below-market pricing

It’s not the right answer if you’re earning above the joint income cap, already own property, or shopping above RM500,000. It’s also worth pausing if your job is unstable — borrowing 110% with thin savings is risky if your income stream isn’t reliable.

Frequently Asked Questions About SRP

What is the maximum property price under SRP?

RM500,000. Property value is assessed at the lower of purchase price or bank-appraised market value. Properties priced above RM500,000 cannot be financed under SRP.

Can I apply for SRP if I’m self-employed?

Yes, but documentation requirements are stricter. You’ll need SSM business registration (if applicable), 12 months of bank statements, latest income tax returns, and a Commissioner of Oaths declaration. Many self-employed buyers find SJKP MADANI is a better fit because it’s specifically designed for irregular income.

What is SRP in salary?

For Skim Rumah Pertamaku (SRP), salary refers to your gross monthly income before deductions. To qualify, your income must generally be:

- Up to RM5,000 for individual applicants

- Up to RM10,000 combined for joint applicants (spouse)

Your housing loan approval will still depend on the bank’s assessment of your financial situation.

Is there an application fee for SRP?

No. SRP itself charges no fee, and the Cagamas guarantee is provided at no cost to the borrower. You pay the bank’s standard processing fees and any property-related costs, but nothing extra for SRP participation.

Can I rent out my SRP-financed home?

No. SRP requires the property to be owner-occupied as your primary residence. Renting out the home breaches the scheme terms and can affect your loan standing.

Are there other government programmes besides SRP that help first-time home buyers?

Yes. Besides Skim Rumah Pertamaku (SRP), Malaysians may also explore initiatives such as the i-Biaya programme, which was introduced to help B40 and M40 households reduce the financial burden of purchasing a home through housing-related assistance and financing support.

Conclusion

Skim Rumah Pertamaku remains one of the most valuable affordable housing options for Malaysian first-time buyers in 2026. For young professionals, newlyweds, and dual-income households earning under RM10,000 combined, SRP solves the biggest barrier to ownership: the down payment. Eligible buyers can move into a home priced up to RM500,000 with almost zero upfront cash, saving between RM50,000 and RM65,000 compared to a regular purchase.

The trade-offs are real. Monthly instalments are higher because you’re borrowing more. You start with negative equity that takes years to resolve. And the income cap excludes many M40 households with combined earnings over RM10,000. These are not reasons to avoid SRP; they simply set realistic expectations for your application.

The smart strategy in 2026 is to stack SRP with other available subsidies: claim the stamp duty exemption (extended until December 2027), explore PR1MA or Rumah Selangorku for below-market pricing, and structure your application carefully through a participating bank that’s currently active in the scheme.