If you’ve watched property prices climb past what your salary can realistically service, you’re not imagining things. Malaysia’s median house price reached around RM486,070 in Q1 2025, while the median monthly household income still sits below RM6,500. The gap is exactly why government affordable housing schemes exist — and PR1MA Malaysia 2026 remains one of the most accessible routes for middle-income Malaysians who want to own rather than rent.

This guide covers everything you need to know to apply this year: who qualifies, what PR1MA homes actually cost, how the application process works through the official portal, what Budget 2026 changed for buyers, and how PR1MA compares to alternatives like Rumah Selangorku. We’ve also included a realistic look at the drawbacks — balloting delays, moratorium restrictions, and slower capital appreciation — because skipping those isn’t doing you any favours.

This is for first-time buyers, M40 households, young professionals, and married couples earning between RM2,500 and RM15,000 a month who want a clear path into home ownership without paying private-market premiums.

What Is PR1MA Malaysia?

PR1MA (Perumahan Rakyat 1Malaysia) is a federal affordable housing programme established under the PR1MA Act 2012 and administered by Perbadanan PR1MA Malaysia. Its job is to plan, develop, and deliver homes priced roughly 20% below market value for middle-income Malaysians in urban and suburban areas.

The programme exists because the private market wasn’t producing enough housing in the RM100,000 to RM400,000 range — particularly in cities where M40 households actually need to live. PR1MA fills that gap by working with appointed developers to build homes that are priced and allocated under government rules rather than left to market forces.

A few things make PR1MA distinct from other affordable housing schemes:

- Nationwide coverage. Unlike Rumah Selangorku (Selangor-only) or Residensi Wilayah (Federal Territories only), PR1MA projects are spread across Peninsular Malaysia and Sabah.

- M40-focused. While B40 households can apply, PR1MA’s income cap of RM15,000 makes it the main affordable scheme for middle-income earners.

- First or second home allowed. This is the big one. Most affordable housing schemes (SRP, Rumah Selangorku, Residensi MADANI) are strictly for first-time buyers. PR1MA allows purchase as either a first or second home, as long as you and your spouse don’t own more than one property between you.

- Balloting system. Demand consistently exceeds supply in popular locations, so units are allocated through transparent balloting.

Under the current MADANI government, PR1MA has been integrated into a broader affordable housing ecosystem that also includes Residensi MADANI, Projek Rumah Rakyat (PRR), and the SJKP financing guarantee. PR1MA still operates as a separate brand and corporation, with its own pipeline targeting 25,000 new units across KL, Melaka, Perak, and Penang under the Madani Housing Reform Agenda.

Who Is Eligible for PR1MA in 2026?

PR1MA eligibility 2026 is straightforward but easy to misread. The rules below come directly from PR1MA’s official FAQ at pr1ma.my.

PR1MA Income Requirements

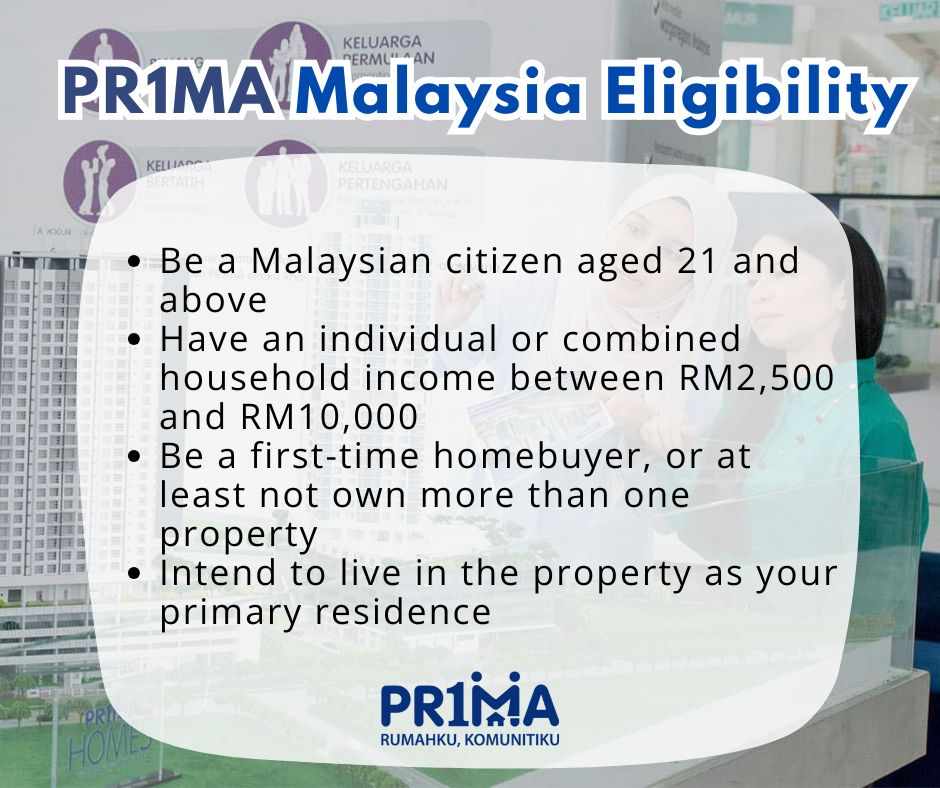

Your gross monthly household income — combining you and your spouse if married — must fall between RM2,500 and RM15,000.

This is a deliberately wide band designed to cover lower M40 households (typically earning RM5,000 to RM8,000) right up to upper M40 households (earning RM12,000 to RM15,000). It also includes some B40 households at the upper end, but most B40 applicants are better served by Rumah Selangorku Type A or Program Perumahan Rakyat (PPR).

A few practical points worth knowing:

- Gross, not net. Use your salary before EPF, SOCSO, and tax deductions.

- Combined for couples. If you earn RM8,000 and your spouse earns RM6,000, your combined household income is RM14,000 — within the cap, but you’d be evaluated as a single household.

- All income counts. Salary, commissions, business income, freelance earnings, and rental from other property all factor in. Underreporting causes problems later when banks pull your statements.

Other Eligibility Requirements

To apply for a PR1MA home, you must:

- Be a Malaysian citizen (no PR holders or foreigners)

- Be at least 21 years old at the time of application

- Not own more than one property between you and your spouse — PR1MA can be your first or second home, but not your third

- Not have previously purchased a PR1MA unit

- Intend to occupy the property yourself (no buying to rent out)

Married couples must register a single joint application. Submitting separately doesn’t double your chances — it disqualifies both submissions.

Documents Required

The PR1MA application is fully online and free. You’ll need to upload:

- MyKad (applicant and spouse if married)

- Marriage certificate (if applicable)

- Latest 3 months’ payslips

- Latest 3 months’ bank statements

- EPF statement (i-Akaun screenshot or KWSP statement)

- Latest income tax return or BE/B form (if available)

- For self-employed: business registration (SSM), commissioner of oaths declaration, and 6+ months bank statements

PR1MA does not charge any application fee, and no agent or third party is authorised to “help” with your application for a fee. This is worth repeating because scammers exploit the demand — anyone offering paid assistance is not legitimate.

PR1MA House Prices and Property Types

Typical PR1MA Property Prices

PR1MA homes are typically priced between RM100,000 and RM400,000, sitting roughly 20% below comparable private-market homes in the same area. Actual pricing varies by location, unit size, and project — landed homes in established suburbs price higher than high-rise units in newer developments.

Once you’re selected through balloting, a booking fee of RM500 applies for completed PR1MA projects. The full purchase then proceeds through standard SPA signing and bank financing.

Types of Homes Available

PR1MA developments include a mix of property types depending on location and project density:

- Apartments and condominiums — most common in urban areas, typically 800 to 1,100 sq ft, 3 bedrooms, 2 bathrooms

- Serviced residences — newer developments in city-fringe locations

- Landed terrace homes — available in selected suburban developments

Most PR1MA projects come with shared facilities — gym, multipurpose hall, surau, playgrounds, and 24-hour security — comparable to mid-tier private developments.

PR1MA Locations Across Malaysia

PR1MA has built projects across most major states, with current and upcoming developments concentrated in:

- Selangor — including completed developments and ongoing projects in the Klang Valley

- Kuala Lumpur — including transit-oriented developments near MRT and LRT lines

- Johor — including projects in Johor Bahru and Iskandar Puteri

- Penang — new developments planned under the 25,000-unit Madani Housing Reform pipeline

- Perak — including Bandar PR1MA Teluk Intan, allocated RM38 million in Budget 2026

- Negeri Sembilan — including Seremban Sentral

- Melaka — part of the new MADANI affordable housing pipeline

- Sabah — Peninsular and Sabah projects share the same eligibility framework

Available stock changes regularly. The full list lives on the PR1MA portal and is worth checking before you finalise your project preferences.

How to Apply for PR1MA Malaysia 2026

The PR1MA application is entirely online. There’s no paper form and no fee.

Step 1 – Register on the PR1MA Portal

Visit pr1ma.my and click “Register”. Create an account using a valid email address and your MyKad number. You’ll receive a unique PR1MA reference number — save this. Every subsequent step references it.

Married couples register once jointly, not separately.

Step 2 – Upload Supporting Documents

Log in to your account and complete your profile. Upload:

- MyKad (front and back, for both applicant and spouse)

- 3 months’ payslips

- 3 months’ bank statements

- EPF statement

- Marriage certificate (if applicable)

All documents should be clear, current, and in PDF or image format. Outdated or unclear documents are a common rejection reason.

Step 3 – Select Your Preferred Project

Browse available PR1MA projects by location, price range, and unit type. You can select multiple preferred projects — this improves your chances since balloting is project-specific.

Be realistic about your selections. Choose locations you’d actually live in and commute from. Rejecting an offer after balloting can affect future eligibility.

Step 4 – Balloting and Offer Process

For projects where applications exceed available units, PR1MA conducts an open, transparent balloting process. Successful applicants are notified by email and SMS.

If you’re selected, you’ll receive an offer letter detailing the unit, price, and next steps. You typically have a specified window (often 14 to 30 days) to accept the offer.

Step 5 – Loan Application and SPA Signing

Once you accept, the financing process begins:

- Conventional bank loan — approval typically takes about 1 month from booking date

- Government loan (LPPSA) — civil servants can apply through LPPSA, with approval taking about 2 months

After loan approval, you’ll sign the Sale and Purchase Agreement (SPA) with PR1MA as the developer. The property is handed over once construction is complete and the Certificate of Completion and Compliance (CCC) is issued.

For new launches under construction, expect handover 24 to 36 months after SPA signing. For completed PR1MA projects, handover is much faster — sometimes within 60 to 90 days.

Budget 2026 Updates for PR1MA Buyers

Budget 2026 (tabled 10 October 2025) introduced several housing measures that directly benefit PR1MA buyers and Malaysian first-time home buyers more broadly.

Direct PR1MA Funding

Budget 2026 allocated specific funding to PR1MA projects:

- RM30.1 million for preliminary works on three PR1MA projects

- RM38 million approved for the Bandar PR1MA Teluk Intan development in Perak

- Around 3,000 PR1MA homes scheduled for completion in 2026

This is alongside the broader MADANI Housing Reform Agenda, which targets 500,000 affordable homes by 2030 with PR1MA contributing 25,000 new units across KL, Melaka, Perak, and Penang.

Stamp Duty Exemption Extended to 2027

The 100% stamp duty exemption for first-time Malaysian home buyers on properties up to RM500,000 has been extended until 31 December 2027. Almost all PR1MA homes fall within this cap, meaning eligible first-time buyers save roughly RM7,500 to RM11,250 in stamp duty on a typical PR1MA purchase.

This applies to both the transfer instrument and the loan agreement — two separate stamp duties, both waived.

Step-Up Financing Scheme

Budget 2026 introduced a new Step-Up Financing programme for buyers aged 21 to 35. Initial monthly instalments start lower and gradually rise over time, easing the early-career cash flow squeeze. The scheme rolls out through participating banks.

LPPSA Ceiling Increased

For civil servants buying PR1MA homes, the LPPSA financing ceiling was raised from RM600,000 to RM1 million, with easier second-loan approvals from Q4 2026. This makes urban PR1MA projects significantly more accessible for government employees.

PR1MA Financing Options

PR1MA homes can be financed through several routes, and choosing the right one materially affects your monthly commitments and approval chances.

Conventional Housing Loans

The most common route. PR1MA partners with major banks including Maybank, CIMB, RHB, Public Bank, Hong Leong, and AmBank. Standard terms apply — 90% margin of finance, tenure up to 35 years or age 70, MRTA/MRTT required.

PR1MA also previously offered a Special End-Financing Scheme (SPEF) through selected banks, designed for buyers who struggled to get conventional approval. Availability of SPEF varies — check directly with banks at the time of application.

SJKP for Self-Employed Buyers

If you’re self-employed, gig-based, or running a small business, SJKP MADANI is your best path to PR1MA approval. The scheme guarantees financing portions banks wouldn’t otherwise underwrite, covering up to 120% of property value for renovation-inclusive packages.

You’ll need 6 to 12 months of bank statements showing regular income flow, business registration (if applicable), and platform transaction history (for ride-hailing or delivery drivers). Full details in our SJKP MADANI guide for self-employed buyers.

Skim Rumah Pertamaku (SRP)

For first-time PR1MA buyers earning up to RM5,000 individually or RM10,000 jointly, Skim Rumah Pertamaku (SRP) provides up to 100% financing through Cagamas SRP Berhad. This effectively eliminates the down payment requirement.

Note: SRP requires you to be a first-time buyer with no other residential property. If you already own a home and are buying a PR1MA unit as a second property, SRP doesn’t apply.

Stamp Duty Savings

Stack the financing schemes with the stamp duty exemption and the upfront savings add up quickly. On a RM400,000 PR1MA home, an eligible first-time buyer using SRP could save around RM40,000 in down payment plus RM10,000 in stamp duty — roughly RM50,000 in real upfront cost. Read our Stamp Duty Guides for eligibility details.

For EPF members, EPF Account 2 withdrawals can also be used for the down payment legal fees and other eligible housing-related expenses through the EPF Members Investment Scheme.

Pros and Cons of Buying a PR1MA Home

Advantages

Below-market pricing. PR1MA homes are typically priced 20% below comparable private-market homes in the same area. For an M40 buyer priced out of the private market, this is the main reason the scheme exists.

Strategic locations. Most PR1MA developments are positioned near public transport, schools, hospitals, and commercial centres. Newer projects are increasingly placed along MRT and LRT corridors.

Government-backed programme. PR1MA operates under the PR1MA Act 2012 and is administered by a federal corporation. All projects are protected under the Housing Development Act (HDA), with stronger buyer protections than informal private developments.

Better financing access. PR1MA buyers can stack SJKP, SRP, LPPSA (for civil servants), and the stamp duty exemption — multiple subsidies that aren’t all available for private market purchases.

First or second home eligibility. Unlike most affordable schemes, PR1MA allows you to buy as a second home. This is useful for buyers who already own a small starter property and want to upgrade to something more suitable without losing access to subsidised pricing.

Disadvantages

Balloting system. High-demand projects in popular locations are oversubscribed. Even with a strong application, you may not be selected. Plan to apply for multiple projects to improve your odds.

Moratorium restrictions. PR1MA homes cannot be sold or transferred within a moratorium period from the SPA date. Sources differ on the current length — PR1MA announced a reduction from 10 years to 5 years back in 2017, but several recent property law guides still cite 10 years. The exact term varies by project and policy era. Always check the moratorium clause in your specific SPA before signing.

Limited unit availability. Total PR1MA delivery has been slower than the original 1-million-unit target set when the programme launched. Budget 2026 expects only ~3,000 new completions in 2026, against demand that runs into hundreds of thousands.

Slower capital appreciation. Because PR1MA homes are priced below market value and have moratoriums limiting resale, capital gains potential is more limited than private properties. If you’re buying primarily for investment returns, PR1MA is not the right scheme.

Project delays. Some PR1MA projects have experienced construction delays — sometimes by 12 to 18 months. Most stalled projects have eventually been completed, but the risk exists for new launches.

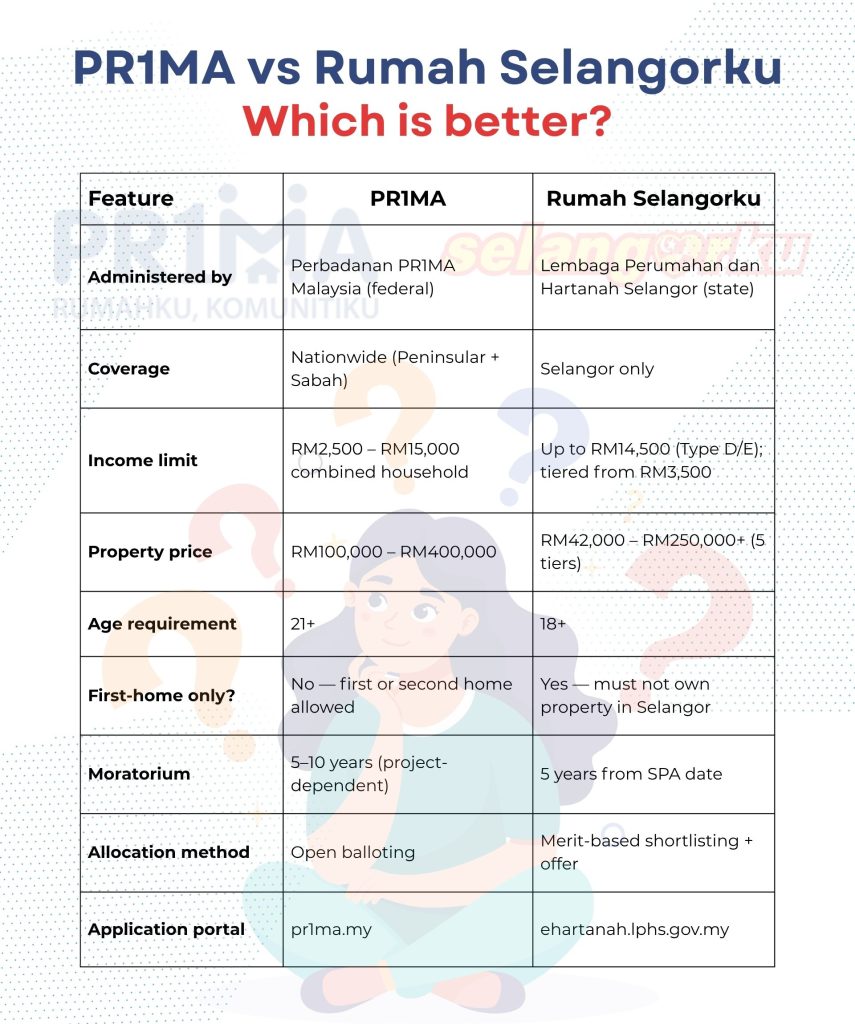

PR1MA vs Rumah Selangorku: Which Is Better?

Both are affordable housing schemes targeting middle-income Malaysians, but they’re built around different rules.

When PR1MA Wins

- You live outside Selangor (Johor, Penang, KL, Perak, Negeri Sembilan, Sabah)

- You already own one property and want to buy a second

- You’re in upper M40 (income RM12,000 to RM15,000) and want a higher-quality urban home

- You want a wider geographical range of project options

When Rumah Selangorku Wins

- You’re a Selangor resident with no property in the state

- You’re in B40 or lower M40 (Type A, B, or C tiers under RM150,000)

- You want a shorter, clearer moratorium period

- You prefer merit-based allocation over open balloting

For a detailed breakdown of Rumah Selangorku eligibility, income limits, house types, prices and application steps, read our complete guide on Rumah Selangorku 2026: Eligibility, Price & How to Apply.

Is PR1MA Still Worth It in 2026?

Honestly: it depends on your situation.

PR1MA is genuinely useful if you’re an M40 household in a city where private property prices have run ahead of your earning power. The 20% below-market discount, combined with the SJKP and stamp duty stacking introduced under Budget 2026, makes the total upfront cost meaningfully lower than buying privately.

It’s worth applying if you’re:

- An M40 household earning RM6,000 to RM15,000 looking for urban housing

- A young professional building career income and want to lock in pricing before further appreciation

- A first-time buyer who needs every available subsidy stacked to make ownership realistic

- An urban family wanting a 3-bedroom unit near MRT, schools, and commercial areas

It’s probably not the right fit if you’re:

- A B40 household earning under RM3,500 — Rumah Selangorku Type A, RMR, or PPR are better matches

- A short-term investor looking for capital gains within 5 years (the moratorium kills the business case)

- Someone who needs immediate possession (most PR1MA projects launch with 24-36 month construction timelines)

The honest 2026 outlook: PR1MA is no longer the centrepiece of Malaysia’s affordable housing strategy that it was in 2015–2018. It’s been folded into a broader MADANI Housing Reform Agenda alongside Residensi MADANI, PRR, and SJKP. New supply is targeted but limited. The scheme still works — but you’ll need patience, multiple applications, and realistic expectations on timeline.

For a full side-by-side comparison covering eligibility, financing options, and how to choose, see our main guide to affordable housing schemes in Malaysia 2026.

Frequently Asked Questions About PR1MA

What is the PR1MA income limit in 2026?

Applicants generally need a monthly household income between RM2,500 and RM15,000 to qualify for PR1MA Malaysia 2026.

Can I apply for PR1MA if I already own a property?

Yes — PR1MA generally allows purchases for a first or second home only. Applicants or their spouse should not own more than one property.

Is PR1MA only for first-time buyers?

First-time buyers are prioritised, but certain second-home purchases may also qualify depending on eligibility requirements.

Can I rent out my PR1MA home?

No. PR1MA homes must be owner-occupied throughout the moratorium period and typically beyond, depending on terms. Renting out the unit breaches the SPA and can lead to enforcement action.

How much are PR1MA homes?

Prices typically range from RM100,000 to RM400,000 depending on project location and property type.

Can foreigners buy PR1MA homes?

No. PR1MA homes are generally reserved for Malaysian citizens only.

Conclusion

PR1MA Malaysia 2026 remains one of the country’s most important affordable housing programmes for middle-income households seeking quality homes at manageable prices.

With support from Budget 2026 initiatives, expanded financing access through SJKP, and ongoing government efforts to improve housing affordability, PR1MA continues to provide meaningful opportunities for Malaysians looking to own an affordable home.

Before applying, compare available projects, financing options and alternative housing schemes carefully to ensure you choose the right property for your long-term needs.